The JP Morgan Shock

The entire world has forgotten about or ignored what could be the upcoming "shock" that puts the global financial system in severe jeopardy. To make matters much, much worse - I don't think anyone even has a clue as to what is really happening. Investors, economists, financial powerhouses, top business executives, politicians, lawmakers, consumers, students, governments, and even central banks are completely confused. None of them are expecting what I will describe below.

There

is one event that may ultimately solve the mystery of the global

economy. This event would not only plunge the economy back into a deep

recession and lose investors hundreds of billions of dollars, but it

could bring about the collapse of some of the world's largest financial

institutions and even render central bank stimulus and QE completely

ineffective and futile. This event is by no means a guarantee; its

probability is even likely under 5 percent. But this event has all the

necessary ingredients to culminate into a major panic. Together with

slowing global economies and an extremely unstable financial system,

this could be the next Lehman Brothers.

There

is one event that may ultimately solve the mystery of the global

economy. This event would not only plunge the economy back into a deep

recession and lose investors hundreds of billions of dollars, but it

could bring about the collapse of some of the world's largest financial

institutions and even render central bank stimulus and QE completely

ineffective and futile. This event is by no means a guarantee; its

probability is even likely under 5 percent. But this event has all the

necessary ingredients to culminate into a major panic. Together with

slowing global economies and an extremely unstable financial system,

this could be the next Lehman Brothers.This event is JP Morgan's huge trading mistake. The massive losses that were racked up starting in April and May 2012 are by no means over. What has been represented by JP Morgan as a trading mistake and "hedging" strategy with an initial estimated loss of $2 billion, was really a leveraged and speculative bet that could soon infect JP Morgan's entire portfolio and result in losses of $100 billion.

The Global Economy and Huge Underlying Risks

Most investors already know about the very weak economic growth, European financial crisis, Chinese slowdown, Middle East tensions, and dangerous Fed actions. All are huge threats and may drag the global economy into a double-dip recession. But most investors don't know if the fears are overblown; they don't know if central banks will be successful in boosting the economy; and they don't know the real risks out there. Most investors are either overly-optimistic, over-confident that they will be able to pull their money out quickly, following the crowd, or simply taking way too much risk unnecessarily. After a 115% + rally, and only 7% away from the all-time stock market highs, it's just not worth staying invested right now.

This was my warning to my friends on September 25, 2012:

All of the above reasons are absolutely enough to crush this market, but guess what? It could get even worse.Take your money out of stocks and gold NOW!!!

$SPY $GLD $AAPL $FB $GOOG $MCD $CAT $JPM

Way too much risk, stock market is only 7% away from the all-time highs (and the economy is nowhere near where it was), Apple has failed to stay above $700 and will potentially never make new highs ever again, Google might have just put in a top, Facebook continues to fail, China is slowing down tremendously and could enter recession, Europe has a financial crisis that is still unresolved, global growth and manufacturing is slowing (already at recession levels), massive debt could lead to financial collapse, the US Dollar is getting stronger, commodity prices are falling after over-speculation, oil prices failed to stay above $100 and signal a deflationary recession, and the Fed's actions have given investors too much confidence when they might not work at all.......Just not enough reward at all for the massive risk that you'd be taking.

JP Morgan Loss

JP Morgan announced that its Chief Investment Office made a terrible trading error and lost $2 billion. The company said that the loss was due to a failed "hedging" and "protection" strategy and blamed it on trader Bruno Iksil, the "London Whale". At first, the company tried to deny or downplay these very negative rumors in order to prevent any panic. But by May 2012, losses of $2 billion were reported and the stock had lost a third of its value in two months, from early April to early June. On an emergency conference call, JP Morgan CEO Jamie Dimon announced that the strategy was "flawed, complex, poorly reviewed, poorly executed, and poorly monitored."

Jamie Dimon was called to testify in front of the Senate, and investigations were initiated by the Federal Reserve, the SEC, and the FBI. In July, the total loss was updated to $5.8 billion and the firm announced that they could total $9 billion under worst-case scenarios. But the problems have still not been solved! JP Morgan is still not out of the trade, and all of the investigations and testimonies have still not uncovered exactly what the trades were, how they resulted in such massive losses, and why such severe mistakes were not caught by top management.

It appears that the losses are still increasing and that JP Morgan is hiding a lot of important information. It is absolutely possible that a number of traders, risk managers, and even Jamie Dimon himself have engaged in illegal activities, misrepresented the real situation, and even lied to the public.

What's Really Happening?

- The Trades

Trade #1 was a smart hedge betting against the global economy, by having bearish positions on junk bonds (JNK) - one of the riskiest asset classes most sensitive to the condition of the economy. This position was a very good hedge because JP Morgan needs to protect itself from a potential economic downturn. If the economy deteriorated and stocks fell, JP Morgan would at least make up some losses by profiting from these bearish bets.

Trade #2 is where the real trouble stems from. Instead of hedging through bearish positions, Trade #2 actually bets on continued economic strength. Trade #2 was a bet that investment-grade bonds will not default - that strong corporations will continue to be financially stable and be able to pay off all of their obligations. JP Morgan's bet was that credit markets would strengthen. To make matters even worse, Trade #2 was based on the position that 2012 should be protected but that 2013-2017 would be safe (buying CDS protection for 2012, selling CDS protection out to 2017). In other words, JP Morgan was now betting that investment grade bonds would not default from 2013 to 2017. Moreover, Trade #2 was much bigger than Trade #1.

- How They Lost

On the other hand, if economic conditions declined, JP Morgan would profit from its short position in junk bonds (which would be hard hit by a slowdown) but would lose on its long positions in investment-grade bonds (which would now be at greater risk of default). Because Trade #2 was much bigger than Trade #1, deteriorating economic conditions would result in a large loss.

JP Morgan's trades were a terrible "hedge" because they were much more geared for an improvement in economic conditions than for a deterioration. Therefore, when world financial markets fell into a slight panic over Europe's financial crisis and slowing global growth, JP Morgan lost billions of dollars on their trades. And it's not over.

Why They're Lying

There is a good chance that legal actions will soon follow. Not only did the Chief Investment Office make very serious trading errors and failed to oversee the trouble that was going on, but there is a fair possibility that a number of individuals in top-level management positions knew what was happening and failed to act. In fact, the CIO (Ina Drew), Chief Risk Officer (Irvin Goldman), and others have already been forced to resign. In my opinion, JP Morgan and a number of individual in high-level management have engaged in market manipulation, public misrepresentation, and conflicts of interest.

- "Hedge." First, calling these botched trades a "hedge" is hugely misleading and even a lie; these trades were not "protection," but an outright bullish and speculative bet on a European resolution and strength of the credit markets. JP Morgan made a massive bet on improving economic conditions instead of rightfully protecting itself from the threats of a recession.

Monday, May 21, 1:35 PM JPMorgan's CIO losses can't be described "in any way as a hedge," says hedge fund giant Michael Platt, whose BlueCrest capital was on the other side of the trade. "It's a trading loss. They deliberately put the positions on." "They're not out of those positions," he says and will face further losses if Europe continues to deteriorate.

Source: Seeking Alpha, Market Currents

- Hiding Losses. Second, it appears that JP Morgan attempted to hide these losses from the public by either denying or minimizing early reports. Finally, when losses grew too large to hide, the company reported a $2 billion loss. Then, after investors had some time to digest the $2 billion loss reported in May, JP Morgan updated the loss to $5.8 billion in July.

- Misrepresenting Financial Results. Third, it is possible that JP Morgan attempted to hide the losses and manipulate investors by retroactively updating financial results, after it misrepresented them more positively. On July 13, 2012, it announced that it had a $4.4 billion loss in the second quarter and a "recalculation" of first quarter results that resulted in a $1.4 billion loss. To me, it looks like JP Morgan pushed off announcing the losses until after first quarter results were announced, and then tried to quietly tuck some of those losses into Q1 only afterwards - when investors weren't paying much attention. To me, it looks like JP Morgan has been trying to cover up its mistakes.

- Faulty Accounting and Valuation. Fourth, JP Morgan manipulated valuations and attempted to decrease the reported loss through faulty accounting standards - valuing thinly-traded positions as more marketable, failing to discount for illiquidity, using incorrect price estimates, and not updating changes in valuations (ZUCKERMAN, GREGORY; DAN FITZPATRICK (August 3, 2012). "J.P. Morgan 'Whale' Was Prodded Bank's Probe Concludes Trader's Boss Encouraged Boosting Values of Bets That Were Losing").

- Conflicts of Interest. Fifth, there are major conflicts of interest at JP Morgan. Not only is CEO Jamie Dimon a board member of the Federal Reserve Bank of NY (why is a top bank CEO so heavily influential on a government institution?), but the biggest campaign donor to many members on the Senate's banking committee - JP Morgan Chase. (Huffington Post, JP Morgan Chase and The Senate Banking Committee Are Best Friends).

- Pointing The Blame. Finally, even though JP Morgan has placed the blame on the "London Whale" and the Chief Investment Office, it is CEO Jamie Dimon who deserves a lot of the blame as well. It is the role of the CEO to oversee what goes on and even to sign off on financial documents that they are accurate (Sarbanes-Oxley). Dimon told lawmakers that the loss was an "isolated incident," but it is more likely that there is much more brewing under the surface.

The $5.8 billion loss that has officially been announced is by no means the final count. Not only have we seen the loss rise from $2 billion to $4 billion to $5.8 billion, but JP Morgan still hasn't exited from its positions. There are a number of reasons why this loss could quickly spiral out of control.

- Still Not Out of Bets. The official announced losses are "only" $5.8 billion, but JP Morgan still hasn't exited from all of its risky positions. In fact, even though JP Morgan's losses have been estimated to be as much as $9 billion under worst case scenarios, this is according to JP Morgan's own internal report. Why should we believe what JP Morgan tells us? Obviously they underestimate their own losses.

Unwinding these bets could put JP Morgan at tremendously high risk:

J.P. Morgan's decision to move slowly in unwinding the positions highlights a painful dilemma for the company and Chief Executive James Dimon: The bank can move slowly and risk being bled by small but regular losses over time, or it can attempt to close out the trades sooner but face potentially larger losses. Moving slowly also holds risks if the market turns sharply against the bank in the near term.

Source: WSJ: JP Morgan Struggles To Unwind Huge Bets

- Sold Protection Maturing in 2017. Perhaps the dumbest move for JP Morgan was its failure to protect itself from a recession or economic slowdown. Instead of buying protection, JP Morgan actually sold protection. Though it bought protection for 2012, it sold protection for 2013-2017 - definitely not a position that would save it if a recession took hold. If economic conditions deteriorate, JP Morgan is in a tremendously dangerous position; it not only failed to protect itself for the next few years, but it even made bullish bets by selling that protection. If it can't unload its positions soon, an economic slowdown could wipe out its entire portfolio as the 2013-2017 protection soars in value and blows up in JP Morgan's face (the positions lost JP Morgan a minimum of 24% in just over a week - WSJ, ibid).

- Regulators Still Haven't Figured It Out. Regulators such as the OCC and SEC have attempted to find out exactly what has happened and how much risk is still out there, but they have likely been looking at "the same models that the bank itself was using (WSJ, ibid.)." It seems that the regulators themselves still have a lot to find out, and the $9 billion max-loss estimated by JP Morgan itself is not likely accurate.

- Way More Than $10 Billion At Risk. While Jamie Dimon insists that Iksil (The London Whale) made a risky $10 billion bet in an illiquid debt index, and that this is an "isolated incident," there may be much more at risk than the measly $10 billion.

First, we've already heard that JP Morgan's position in risky, illiquid debt derivatives has had a face value of $100 billion; Iksil's position may have been $10 billion, but somehow JP Morgan attained a $100 billion risk exposure. Second, even if just a $10 billion position was taken, if it is highly-leveraged it could wipe out much of the value of JP Morgan's other assets.

Haven't we learned the lessons of the giant financial collapses of Lehman Brothers, Bear Stearns, Merrill Lynch, AIG, MF Global, and others? Haven't we already seen how leveraged, "isolated" bets can bring down entire corporations? Even if JP Morgan's bet was limited to $10 billion (which it likely wasn't, because we've already heard of the $100 billion in risky positions), its leveraged losses could infect the entire $350 billion CIO portfolio. It is completely possible that the contagion will spread, the $6 billion in losses will continue to grow, the $100 billion in risky positions will collapse, and JP Morgan's $350 billion CIO portfolio will be severely affected.

- Depositors' Money At Risk? It is not even a stretch to say that depositors' money is at risk (Bloomberg). If the botched position is still uncovered, it could potentially infect the rest of the CIO's portfolio - and even wipe out JP Morgan's entire capital base.

"Essentially, JP Morgan has been operating a hedge fund with federal insured deposits within a bank," said Mark Williams, a professor of finance at Boston University, who also served as a Federal Reserve bank examiner.

Source: NYT DealBook, JPMorgan Trading Loss May Reach $9 Billion

- Could Derail Fed's Monetary Policy. If JP Morgan's losses really do begin to escalate, they affect much more than just JP Morgan. As one of the largest "too big to fail" banks, JP Morgan has benefited tremendously from the added liquidity that the Fed has brought to the markets. The Fed's mission was to increase lending, improve banks' balance sheets, and give "easy money" to these institutions in order to boost the economy. There is no doubt that the Fed's stimulus has bolstered companies like JP Morgan , Bank of America (BAC), AIG (AIG), Wells Fargo (WFC), Goldman Sachs (GS), Citigroup (C), and many financials (XLF). But if JP Morgan goes down, the repercussions will be much greater than in 2008. The economy is not ready to deal with another huge shock. This time, the contagion would be much greater, and the government will not have the capacity to protect failing firms. A collapse of a too-big-to-fail bank would destroy confidence and undermine the Fed's monetary policy.

Though it is impossible to predict events exactly, sometimes there are enough clues that point to good or bad news that may soon come. Sometimes there are rumors, improving or deteriorating financials, upcoming catalysts, and a number of hints which signal that momentum is shifting. Sometimes these are positive developments, pointing to an explosive surge in the company's stock, and sometimes these are negative developments, pointing to an upcoming crash. In the case of JP Morgan, there were reasons to watch out.

1. Hedge Funds Take Other Side. In early 2012, hedge funds such as Saba Capital and Blue Mountain Capital made billions by taking the opposite side of the trade when they noticed that JP Morgan was affecting the market and making aggressive bets. Anyone who paid attention could have noticed that something was going on.

2. Jamie Dimon Against Higher Capital Requirements. In June 2011, Dimon became a "Wall Street Hero" when he boldly questioned Bernanke about whether too much bank regulation - especially the higher capital requirements - would affect the economy and prevent a full recovery.

Bernanke didn't have much to say other than that they are doing everything they can to "develop a system that is coherent and that is consistent with banks performing their vital social function in terms of extending credit.""Now we're told there are going to be even higher capital requirements, and we know there are 300 rules coming, has anyone bothered to study the cumulative effect of these things? And do you have a fear-like I do-that when we look back and look at them all, that they will be the reason that it took so long for our banks, our credit, our businesses, and most importantly, our job creation, to start going again? Is this holding us back at this point?"

Source: CNBC, Jamie Dimon Becomes Wall Street s Hero Figure

Wall Street considered Jamie Dimon a hero, but Dimon's rejection of higher capital requirements should have been a warning. Higher capital requirements are a smart and likely effective way of reducing banks' risk-taking. By increasing capital requirements, the banks would be forced to hold more reserves on hand in order to protect them in case of a sudden downturn or financial distress. This is exactly what we need! Without higher capital requirements, banks are just leveraging their money even more - taking way more risk than they can afford.

Jamie Dimon was basically saying: "Please allow us to bet or loan $1000 when we only really have $100." In other words, Dimon wanted an expansion of banks' financial power without having to increase the safety. By decreasing capital requirements, banks would be able to decrease the amount of money they used as collateral - the "money multiplier" would allow banks to essentially create money out of nowhere and increase lending and investments - which helps banks make more profits and would hopefully help boost the economic recovery. However, if anything goes wrong, the billions (or trillions) of dollars of new loans and investments could collapse in value. And if all of these new loans and investments have been made on "margin" through leverage and monetary expansion, there isn't enough capital to cover the losses - their entire business could be wiped out.

If we actually paid attention to what Jamie Dimon said that day, we could have seen that he wanted more leeway and more power for the banks. Perhaps banks needed more power in order to help the economy, but decreasing the capital requirements and giving banks more room for leverage is exactly what leads to huge financial catastrophes like Lehman Brothers. It was obvious that Dimon was paving the way for increased risk-taking by the banks. And that mindset is what ultimately led to this JP Morgan fiasco.

Dimon's actions in June 2011 foreshadowed this trading loss:

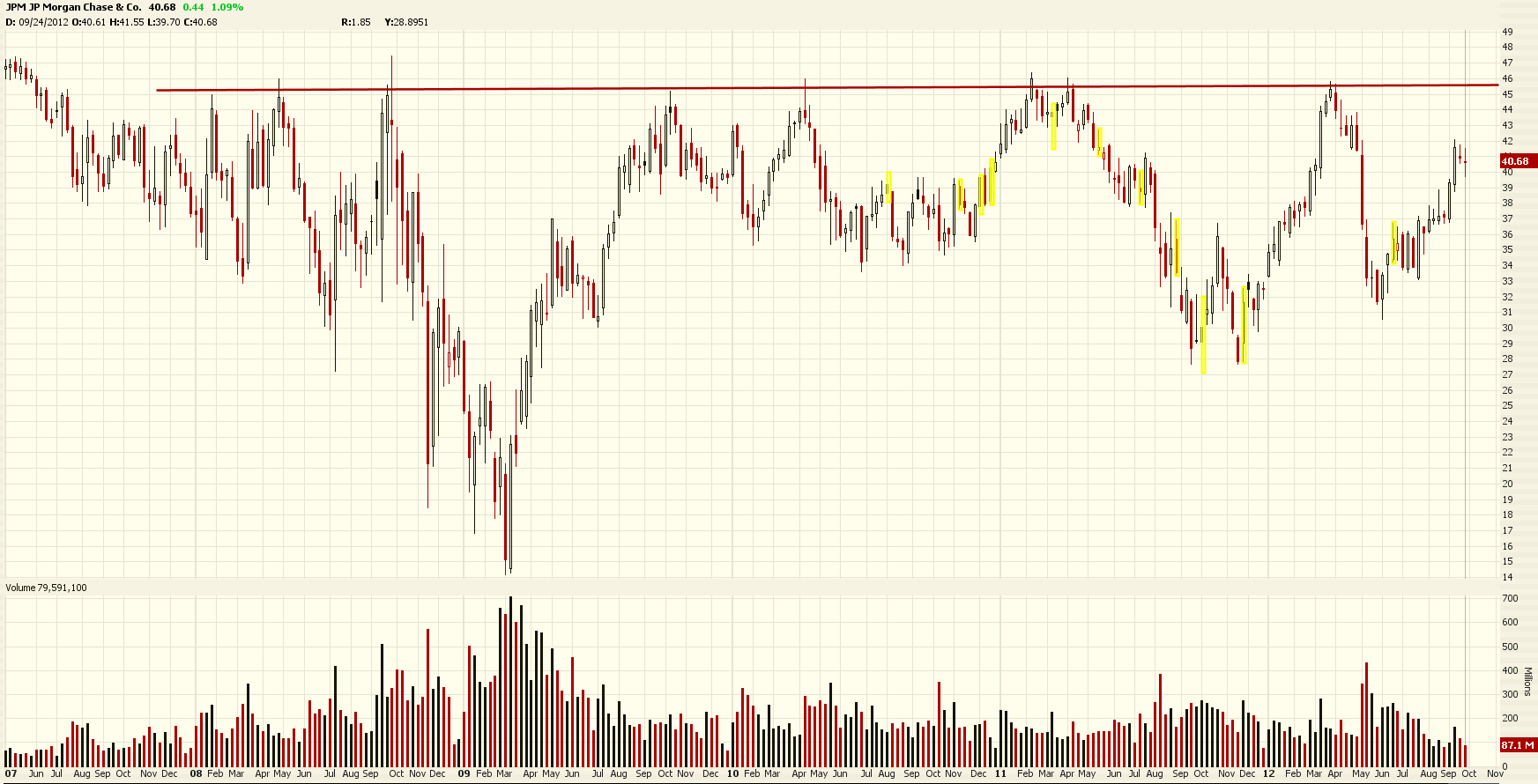

3. Eight Technical Failures. Perhaps the most obvious sign that JP Morgan was about to drop, was the consistent technical failure in the charts. Every time JP Morgan's stock approached $45 or $46, it failed. Looking back all the way to 2007, the $45-$46 level was like a brick wall that completely blocked the stock every time. This could be one of the easiest bets a short-seller could ever make. If you just looked at the 5-year chart of JPM in April 2012, you'd notice that we were approaching major resistance overhead. Every single time we rose to this level, we fell; and in late 2008, we fell from over $45 to almost $14.The enormous loss JPMorgan announced today is just the latest evidence that what banks call "hedges" are often risky bets that so-called "too big to fail" banks have no business making.

-Senator Carl Levin, Michigan (D)

Source: NYT DealBook. SEC Opens Investigation Into JPMorgan s $2 Billion Loss

All one had to do was see if JPM could break above and stay above $46. If it did, JPM would be a decent long position at very low risk, with a brand new support at $45. But if it failed (and it did), JPM would be a good short. This massive resistance was so powerful, that JPM actually failed once again. Not only that, but it failed in late March - investors had over a month to notice this and short the stock! Technicals were signaling a massive warning even before the bad news reached the public.

(Click to enlarge)

Conclusion

All of these facts and clues are still to be determined. JP Morgan may in fact work everything out and escape with under $10 billion in losses. A lot of what I've written is opinion based on the available facts, and the probability of the collapse of a giant financial institution is still extremely low. But there are simply way too many unresolved issues still to be dealt with; there are way too many unanswered questions to be answered by Jamie Dimon and regulators.

JP Morgan was lucky that the bad news came out right before the summer, and that the "summer doldrums" helped investors and lawmakers forget about the massive trouble that may be underway. JP Morgan and CEO Jamie Dimon have been completely silent about this for a few months now, and the stock has recovered all of its losses since the news broke out. Technically, this looks like a "pullback" before the next plunge. The stock may have room to rise, but after such terrible news it is hard to see how it can sustain new highs. To make matters worse, JPM was included in Goldman's Hedge Fund Very Important Position list and Goldman Sachs' VIP List of 50 stocks most important to hedge funds. If JPM suffers, you can bet that most hedge funds, pension funds, and investors will suffer as well.

I repeat: QE and central bank stimulus could turn out to be a great success that saves our economy. But the risks of investing just far outweigh the potential rewards at this point. If you're smart, you'll avoid or short this market and miss out on a maximum 7% upside move if stocks continue to rise (and then get in at minimum risk if we exceed the 2007 highs). By doing so, you'll also save yourself from a devastating 20-50% drop in stocks if the situation deteriorates. I understand we all want to grow our wealth and make money through investing in order to improve our lifestyle, fund our retirement, support our children, and have the ability to do what we want. But at this point, staying long is just being greedy.

Source

banzai7

No comments:

Post a Comment